Japan Real Time Charts and Data

Edward Hugh is only able to update this blog from time to time, but he does run a lively Twitter account with plenty of Japan related comment. He also maintains a collection of constantly updated Japan data charts with short updates on a Storify dedicated page Is Japan Once More Back in Deflation?

Monday, October 29, 2007

Japan Retail Sales September 2007

As in August, Japan retail sales in September 2007 managed to eke out a small (0.5%) year on year increase - according to data released by METI today - but as in August this was largely due to a low base effect, since sales in August and September of 2006 were not exactly spectacular (see chart below). Quarter on quarter sales in July-September were down 0.5% on sales in April-June, an outcome which is not exactly a positive indicator for the up and coming Q3 2007 GDP data.

Friday, October 26, 2007

Japan Industrial Output September 2007

Japan's industrial production fell in slightly September from the record August level, as makers of cars and general machinery cut manufacturing following a slowdown in overseas demand. Production was down a seasonally adjusted 1.4 percent from a month earlier, when it surged 3.5 percent, according to data from the Trade Ministry in Tokyo today.

Claus will probably have a fuller comment on the general Japan economy situation up in the near future, so at this point I would simply note that this reading is hardly a very bad one, since the August level was very high after the increase to cover production lost after the earthquake. On the other hand it is very hard to decide what this industrial data really tells us about what to expect from the up and coming Q3 2007 reading since, apart from slowing export growth, domestic demand remains weak, and additionally so since a recent change in building regulations has caused a delay in home construction, with housing starts plummeting 43 percent - to a 41-year low - in August.

Claus will probably have a fuller comment on the general Japan economy situation up in the near future, so at this point I would simply note that this reading is hardly a very bad one, since the August level was very high after the increase to cover production lost after the earthquake. On the other hand it is very hard to decide what this industrial data really tells us about what to expect from the up and coming Q3 2007 reading since, apart from slowing export growth, domestic demand remains weak, and additionally so since a recent change in building regulations has caused a delay in home construction, with housing starts plummeting 43 percent - to a 41-year low - in August.

Wednesday, October 24, 2007

Japan Exports September 2007

Japan's exports grew at the slowest pace in two years in September as shipments to the U.S. dropped back. In total exports rose 6.5 percent from a year earlier, according to data from the Japanese Finance Ministry released earlier today. At the same time imports declined for the first time in more than three years, helping the trade surplus widen to yet another record.

Shipments to China, the rest of Asia and Europe, however, remained reasonably firm, and this is important given the fact that exports constitute the main engine of the growth for the Japanese economy. Growth in exports to China slowed somewhat, down to an annual 16.5 percent last month from and annual 23.7 percent in August. Asian exports increased at an 8.3 percent rate after climbing by 16.4 percent in August. Shipments to Europe rose 13.2 percent in September after August's 15.5 percent gain.

Now the situation is slighly deceptive given that a significant part of the exports to China, the tigers and emerging Asia (ASEAN) consists of components which will be processed and then re-shipped elsewhere (principally Europe and the US), but still, there is obviously some element of "rebalancing" going on, and it will be interesting to monitor this as we move forward. The vitality of Japanese exports to the EU is hardly surprising given the relative values of the yen and the euro, but it would be interesting to check just how exports to the EU are growing from Singapore, Hong Kong, Taiwan and South Korea (the position vis-a-vis China is already pretty well known I think).

Exports to the US fell 9.2 per cent from a year earlier, and this was the biggest drop since November 2003, a factor which raises fears that subprime problems were taking a toll on Japan’s major export destination. The main component in the fall in US-bound exports was auto shipments, which fell 15.2 per cent from a year earlier. Construction machinery for housing also fell significantly.

Imports fell 3.2 percent in September, the first drop since February 2004, as oil costs declined 12.4 percent from September 2006. In so doing they confounded a consensus forecast for a 2 per cent increase. As a result, the trade surplus expanded by 62.7 per cent to a record Y1,640bn ($14.3 bn), compared with economists’ median forecast for a 47.1 per cent rise to Y1,500bn.

Japan needs export growth if the economy is to rebound from its second-quarter contraction as falling wages keep the lid on spending by consumers at home. Japan’s economy in fact contracted 0.3 per cent in April-June largely as a result of a slump in capital spending, so it will be very interesting to see whether Japan is able to turn this situation around in the July-September quarter, and if it does manage to do this, just how it manages to do so.

Shipments to China, the rest of Asia and Europe, however, remained reasonably firm, and this is important given the fact that exports constitute the main engine of the growth for the Japanese economy. Growth in exports to China slowed somewhat, down to an annual 16.5 percent last month from and annual 23.7 percent in August. Asian exports increased at an 8.3 percent rate after climbing by 16.4 percent in August. Shipments to Europe rose 13.2 percent in September after August's 15.5 percent gain.

Now the situation is slighly deceptive given that a significant part of the exports to China, the tigers and emerging Asia (ASEAN) consists of components which will be processed and then re-shipped elsewhere (principally Europe and the US), but still, there is obviously some element of "rebalancing" going on, and it will be interesting to monitor this as we move forward. The vitality of Japanese exports to the EU is hardly surprising given the relative values of the yen and the euro, but it would be interesting to check just how exports to the EU are growing from Singapore, Hong Kong, Taiwan and South Korea (the position vis-a-vis China is already pretty well known I think).

Exports to the US fell 9.2 per cent from a year earlier, and this was the biggest drop since November 2003, a factor which raises fears that subprime problems were taking a toll on Japan’s major export destination. The main component in the fall in US-bound exports was auto shipments, which fell 15.2 per cent from a year earlier. Construction machinery for housing also fell significantly.

Imports fell 3.2 percent in September, the first drop since February 2004, as oil costs declined 12.4 percent from September 2006. In so doing they confounded a consensus forecast for a 2 per cent increase. As a result, the trade surplus expanded by 62.7 per cent to a record Y1,640bn ($14.3 bn), compared with economists’ median forecast for a 47.1 per cent rise to Y1,500bn.

Japan needs export growth if the economy is to rebound from its second-quarter contraction as falling wages keep the lid on spending by consumers at home. Japan’s economy in fact contracted 0.3 per cent in April-June largely as a result of a slump in capital spending, so it will be very interesting to see whether Japan is able to turn this situation around in the July-September quarter, and if it does manage to do this, just how it manages to do so.

Thursday, October 18, 2007

David Pilling on Koizumi and Reform

Financial Times journalist David Pilling - who is a very able Japan watcher - has a most interesting piece in the FT today. Since he makes some very simple points in a very clear fashion, I will take the unusual step - for this blog at least - of quoting at some length.

David Pilling makes several points which are very well taken. In the first place, he points out that Japan's recent "recovery" is much more the result of strong external demand than it is of structural reforms. Indeed Japan is very dependent on export growth for GDP growth as Richard Katz also explains.

Secondly Japan is now suffering from some form of "reform fatigue", and this will be important as we move forward:

Outside of the labour market and the banking sector - which mainly happened before Koizumi arrived - there has been very little in the way of real structural reform, and even less in the way of "fiscal consolidation". The biggest genuine Koizumi reform was postal privatisation, but this did not start until a year after he left office and will not be completed until 2017.

Lastly, Pilling emphasises, it has been strong external conditions which have given the seemingly positive result, in the Japanese case China, and in the German one Eastern Europe (this part is, of course, my view).

At the end of the day I cannot but agree with David Pilling's concluding remark.

There are, note are, reasons to worry here, and plenty of them. As Pilling would also point out, we are still mired in deflation and there is now real sign of this problem going away.

David Pilling makes several points which are very well taken. In the first place, he points out that Japan's recent "recovery" is much more the result of strong external demand than it is of structural reforms. Indeed Japan is very dependent on export growth for GDP growth as Richard Katz also explains.

Kiichi Murashima, chief economist of Nikko Citigroup in Tokyo, has just returned from London. He did not have much fun. After several meetings with investors in both Japanese government bonds and equities, he concluded: “People are losing interest in Japan.” Lack of enthusiasm stems partly from the fact that Japan’s less-than-exciting growth remains dependent on now-more-uncertain external demand. But underlying the disappointment is a deeper concern that political paralysis resulting from last month’s collapse of Shinzo Abe’s administration will lead to policy seizure.

Superficially, such fears are understandable. Last month Yasuo Fukuda, a 71-year-old man in a grey suit, was hustled into office by a few faction bosses of the ruling Liberal Democratic party. The selection smacked of old-style Japan before Junichiro Koizumi, the last-but-one prime minister, subverted convention by appealing directly to public support.

Secondly Japan is now suffering from some form of "reform fatigue", and this will be important as we move forward:

Worse for the worriers, Mr Fukuda, a consensus-style politician, assumes office at a time of apparent backlash against “Koizumi reforms”. In July the ruling party was punished in upper house elections by voters in poorer parts of Japan, for whom five years of recovery has had little tangible effect.

Outside of the labour market and the banking sector - which mainly happened before Koizumi arrived - there has been very little in the way of real structural reform, and even less in the way of "fiscal consolidation". The biggest genuine Koizumi reform was postal privatisation, but this did not start until a year after he left office and will not be completed until 2017.

There is a misunderstanding about the nature of structural reform and what role, if any, it played in Japan’s recovery. At the best of times, “reform” is a sloppy word used to mean “good change”, a convenient sanctuary for politicians unwilling to concede that not every new law they instigate is beneficial. In Japan, where it has been conflated to mean both fiscal consolidation and deregulation, the term is less illuminating still.

What role did either cutting budgets or pushing deregulation under Mr Koizumi have in boosting growth? Almost none. When he took over during a banking crisis in 2001, he promised to slash government borrowing. Fortunately, he did no such thing. To have done so would have risked tipping the deflation-riddled economy into even deeper recession. He did cut public works budgets. Towards the end of his tenure, he brought overall spending under control and raised revenue through stealth taxes. This may have been good for the long-term health of Japan. But few economists, if any, have argued that it spurred recovery.

Deregulation can accelerate growth. But most Japanese deregulation – for example in the financial and retail sectors – was instigated before Mr Koizumi arrived on the scene.

Lastly, Pilling emphasises, it has been strong external conditions which have given the seemingly positive result, in the Japanese case China, and in the German one Eastern Europe (this part is, of course, my view).

The real key to recovery under Mr Koizumi was the beneficial effect of a booming China on exporters and success in getting banks in shape. Exports were helped further by massive currency intervention to keep the yen low. Even in Japan’s muddled debate, that policy was never classified as reform.

At the end of the day I cannot but agree with David Pilling's concluding remark.

There are legitimate reasons to worry about Japan, not least the failure of wages to rise and consumer demand to stir. But concern that Mr Fukuda will tear up Mr Koizumi’s reform manual is not one of them.

There are, note are, reasons to worry here, and plenty of them. As Pilling would also point out, we are still mired in deflation and there is now real sign of this problem going away.

Friday, October 12, 2007

Japan August 2007 Consumer Confidence Index

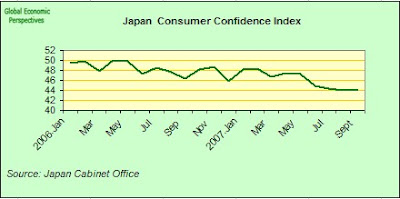

Japanese household sentiment stayed stuck hoevering around a three-year low in September, and there is little indication in the latest consumer confidence index that Japanese consumer spending is likely to accelerate any time soon. The sentiment index that measures confidence among households with two or more people edged up to 44.1 points last month from 44 in August, arresting what had been a four-month slide, the Cabinet Office said in Tokyo today. Although the slide has halted the level is still way below the 50 mark which differentiates a passimist majority from an optimist one.

This continuing gloom among consumers suggests spending at home is unlikely to sustain Japanese growth should a global slowdown damp exports. Household confidence has been hit by sliding pay, a tax increase and the government's loss of pension records. Now families are also starting to feel the pinch from rising prices of food products like bread and instant noodles, even why technology services like mobile phone costs continue to fall, and the overall price index remains in negative deflationary territory.

All the components of the index - including employment - are well down on the levels registered at the end of 2006.

And you can now find this kind of quote - from Bloomberg - all over the place:

The worst part is that this assessment is probably realistic: it isn't going to get any better. This is how a rapidly ageing society works. The novelty is, perhaps, that this time it is finally sinking in.

You can also find a lot of this sort of commentary:

This is the general hope, but it is a big white and empty one as far as I can see from the evidence, since it is the kinds of job which Japan is creating - given its ageing workforce - which is being reflected in those agregate wages, and nothing much is likely to change in this department anytime in the forseeable future.

This continuing gloom among consumers suggests spending at home is unlikely to sustain Japanese growth should a global slowdown damp exports. Household confidence has been hit by sliding pay, a tax increase and the government's loss of pension records. Now families are also starting to feel the pinch from rising prices of food products like bread and instant noodles, even why technology services like mobile phone costs continue to fall, and the overall price index remains in negative deflationary territory.

All the components of the index - including employment - are well down on the levels registered at the end of 2006.

And you can now find this kind of quote - from Bloomberg - all over the place:

"The bad news about pensions and taxes is just adding up,'' said Martin Schulz, senior economist at Fujitsu Research Institute in Tokyo. Wages aren't rising even as companies' profits are increasing, ``so people are thinking: it's not going to get any better than this."

The worst part is that this assessment is probably realistic: it isn't going to get any better. This is how a rapidly ageing society works. The novelty is, perhaps, that this time it is finally sinking in.

You can also find a lot of this sort of commentary:

The country's largest companies expect the worst labor shortages in 15 years, according to the central bank's quarterly Tankan business survey. Bank of Japan Governor Toshihiko Fukui has said that the demand for workers will start to drive wages higher, supporting consumers.

This is the general hope, but it is a big white and empty one as far as I can see from the evidence, since it is the kinds of job which Japan is creating - given its ageing workforce - which is being reflected in those agregate wages, and nothing much is likely to change in this department anytime in the forseeable future.

Thursday, October 11, 2007

Not Much News from the BOJ

Today's meeting in the BOJ did not bring much news from the eastern shores of Asia as the overnight rate was kept at 0.5%. Relative to the mixed signals from the economic readings on August there is not much new data available apart from Ken Worsley's note that one of the leading economic sentiment indices (Economy watchers) fell for a sixth consecutive month. As for the meeting itself the BOJ continued, like the ECB, to cite the ongoing turmoil in financial markets as a reason for maintaining the rate*.

The Bank of Japan kept interest rates unchanged today because it needs more time to gauge the effect of the U.S. subprime-mortgage crisis on the global economy, Governor Toshihiko Fukui said.

Policy makers kept the benchmark overnight lending rate at 0.5 percent, the central bank said in a statement today in Tokyo. The decision was by an 8-1 vote, with Atsushi Mizuno the sole advocate for an increase for a fourth consecutive meeting.

Fukui said the central bank had ``seen some improvement in global financial markets, yet some uncertainties remain.'' Waning confidence and investment at small businesses is also a risk to economic growth, board members Kazumasa Iwata and Miyako Suda said in the past month.

(...)

`The biggest uncertainty right now is how much U.S. housing prices will fall,'' he said. Japan's exports will remain firm as shipments elsewhere offset any drop in U.S. demand.

Another interesting news slip on Japan today was that Moody actually chose to upgrade the Japanese sovereign debt rating as what can only be interpreted as a signal of good faith directed at the new prime minister Yasuo Fukuda.

Japan's credit rating was raised one level to A1 by Moody's Investors Service, which said it's confident the government will reduce the world's largest debt.

The increase in the long-term local currency rating to the fifth-highest investment grade was the first by Moody's since it assigned Japan the top Aaa grade in 1993. The rating had been cut four times since 1998 as the nation's borrowings swelled to 1.5 times the size of the economy.

Prime Minister Yasuo Fukuda is tackling Japan's debt through spending cuts, Moody's Senior Vice President Thomas Byrne said in a statement. Japan owes 834.4 trillion yen ($7.1 trillion), the equivalent of the economic output of Asia- Pacific's next 16 largest economies combined.

Here at Alpha.Sources I certainly hope that Fukuda will be able to bring the house back in order on the back of the mess left behind by Abe. Yet, when it comes to the debt situation itself I fear that my hope is nothing but a fools kind, at best. In this way you cannot help but feel that the credit, as it were, extended to Fukuda from Moody represents a burden which may too hard to carry but here is definitely to hoping. Another perspective related to Japan's debt is this ...

``My view is that the downgrade many years ago was inappropriate because even though Japan's debt is huge, it's held by the Japanese and they are not about to dump those bonds,'' said Masaaki Kanno, chief economist at JPMorgan Securities Japan Co. ``So the upgrade is a natural response.''

Now, while I would like to reiterate here what Kanno says we also need to remember that the debt needs to be served no matter who holds the debt. This means that higher interest rate all things equal will make the servicing of the debt much higher and essentially impossible from the point of view of what many calls 'normalized' Japanese rates. Lastly, in the most unwanted event of a default (also merely on a part of the debt) we also need to remember how this actually might serve to be a disadvantage event for Japan since this would, with one devastating sweep, lower the stock of domestic savings in Japan which in the current long term economic situation is wholly unwanted and essentially would constitute a disaster.

* All quotes are from Bloomberg

Japan August 2007 Machinery Orders

Just a brief note on future orders in the key machinery sector. Machine orders declined by a more-than-expected 7.7 percent in August, after gaining 17 percent the month before, according to data from the Cabinet Office in Tokyo today. This is not quite as bleak a picture as it appears, since in fact overseas orders rose 23% over what had been a rather low level in July. To get some idea of where we are here are the various indexes:

So August was it seems a record month for overseas machinery orders. It now remains to be seen what the picture looked like in September, when we eventually get the data.

So August was it seems a record month for overseas machinery orders. It now remains to be seen what the picture looked like in September, when we eventually get the data.

Tuesday, October 09, 2007

Japan Economy Watchers Index September 2007

The Economy Watchers index, which is a gauge of Japanese domestic demand based on a survey of workers who deal with consumers, fell for a sixth consecutive month in September, to 42.9, down from 44.1 in August, according to the Japanese Cabinet Office in Tokyo today (Japanese only). A number less than 50 means pessimists outnumber optimists.

Today's report, which is the first piece of consumer-related data we have for September, suggests Japanese consumer spending may may fail to support growth should exports cool as a result of the global slowdown. Sentiment among consumers, whose spending accounts for more than half of gross domestic product, has been battered by sliding pay, a tax increase and the government's loss of pension records.

As we can see, in the sub indexes sentiment among retailers fell 2.2 points to 40.4 - its lowest level in four years, while confidence at food-related businesses tumbled 7 points to 36.3, the worst since February 2003.

Wages have dropped in seven of eight months this year and have fallen around 10 percent in the past decade. Pay rose 0.1 percent in August, but this is in part explained by workers putting in overtime hours to make up for a production slump caused by an earthquake in the previous month.

Consumer confidence dropped in August to its lowest level in almost three years and stocks also had a downward correction. A withdrawal of tax rebates in June and the government's admission in May that it lost pension records may also be taking a toll on sentiment.

Today's survey showed shopkeepers expect spending to slow in the next two to three months, while the outlook index fell to 46 in September from 46.5 in August.

Sentiment indexes are often hard to read, and need to be thought about in junction with other "real" economic data. But when we put these results, which really do seem to be fairly clear, together with what we already know about weak Japanese earnings (despite the apparently tight Japanese labour market), weak consumption, and the export dependence of the Japanese economy, all the data does seem to be pointing in the same direction: as I suggest here (and see also Claus here), the danger of a recession in Japan is now real and strong.

Today's report, which is the first piece of consumer-related data we have for September, suggests Japanese consumer spending may may fail to support growth should exports cool as a result of the global slowdown. Sentiment among consumers, whose spending accounts for more than half of gross domestic product, has been battered by sliding pay, a tax increase and the government's loss of pension records.

As we can see, in the sub indexes sentiment among retailers fell 2.2 points to 40.4 - its lowest level in four years, while confidence at food-related businesses tumbled 7 points to 36.3, the worst since February 2003.

Wages have dropped in seven of eight months this year and have fallen around 10 percent in the past decade. Pay rose 0.1 percent in August, but this is in part explained by workers putting in overtime hours to make up for a production slump caused by an earthquake in the previous month.

Consumer confidence dropped in August to its lowest level in almost three years and stocks also had a downward correction. A withdrawal of tax rebates in June and the government's admission in May that it lost pension records may also be taking a toll on sentiment.

Today's survey showed shopkeepers expect spending to slow in the next two to three months, while the outlook index fell to 46 in September from 46.5 in August.

Sentiment indexes are often hard to read, and need to be thought about in junction with other "real" economic data. But when we put these results, which really do seem to be fairly clear, together with what we already know about weak Japanese earnings (despite the apparently tight Japanese labour market), weak consumption, and the export dependence of the Japanese economy, all the data does seem to be pointing in the same direction: as I suggest here (and see also Claus here), the danger of a recession in Japan is now real and strong.

Wednesday, October 03, 2007

Feldman on Japan

Over at the Japan Economy and News blog Ken Worsley alerts us to a notification he got from Bloomberg about a recent interview conducted by Tom Keene with Morgan Stanley's Robert Alan Feldman on the political and economic situation in Japan. Here at JEW we have on several occasions applauded Feldman's work on Japan and its ageing problem. For my own part many of my notes on Japan have been directly inspired by Feldman's work.

You can get the interview here.

I am listening to it as I type but in light of the high standards maintained by Tom Keene and Feldman's brilliant insight there is really only one message to take away from this ... go get it!

At a later point I hope that I will be able to write a fuller commentary on what Feldman is actually saying.

You can get the interview here.

I am listening to it as I type but in light of the high standards maintained by Tom Keene and Feldman's brilliant insight there is really only one message to take away from this ... go get it!

At a later point I hope that I will be able to write a fuller commentary on what Feldman is actually saying.

Monday, October 01, 2007

September Tankan and August Earnings

The September Tankan index of sentiment at large manufacturers came in with a more or less neutral reading. At 23 it was unchanged from June. Since people were expecting worse this is being generally well received, but beyond that I have little more to say, since we need to await data.

Also out today was the Provisional Report of the Monthly Labour Survey for August 2007, and here I do have rather more to say. As I keep stressing, to understand what is going on in Japan you need to look beyond the headlines to the actual data. And one more time Bloomberg haven't disappointed me.

First off it was total cash earnings that were up 0.1% y-o-y, and not real wages which were actually up rather more at 0,4% (I really have no idea how they simply manage to get everything wrong at the level of detail). So here is the chart of monthly changes on a year on year basis.

But... and here comes the really important rub in all of this... if you go and check the time series for the index you will find that August 2006 was a bad month for earnings, since total earnings were down 0,2% on a year earlier in August 2006, so even this meagre increase in August is hard to interpret, and certainly doesn't tell you that "unemployment near a nine-year low is beginning to spur wages" which I think was the point behind the Bloomberg story.

Here is the index itself for what it is worth, although as you can see with bonuses and other items there is a lot of monthly movement and it must be very hard to establish the trend here.All the same, when you look at it in context, August 2007 doesn't seem to me to be a particularly exciting reading.

Also out today was the Provisional Report of the Monthly Labour Survey for August 2007, and here I do have rather more to say. As I keep stressing, to understand what is going on in Japan you need to look beyond the headlines to the actual data. And one more time Bloomberg haven't disappointed me.

Unemployment near a nine-year low is beginning to spur wages in the world's second-largest economy. Wages increased 0.1 percent in August, the Labor Ministry said today, the first gain in nine months.

First off it was total cash earnings that were up 0.1% y-o-y, and not real wages which were actually up rather more at 0,4% (I really have no idea how they simply manage to get everything wrong at the level of detail). So here is the chart of monthly changes on a year on year basis.

But... and here comes the really important rub in all of this... if you go and check the time series for the index you will find that August 2006 was a bad month for earnings, since total earnings were down 0,2% on a year earlier in August 2006, so even this meagre increase in August is hard to interpret, and certainly doesn't tell you that "unemployment near a nine-year low is beginning to spur wages" which I think was the point behind the Bloomberg story.

Here is the index itself for what it is worth, although as you can see with bonuses and other items there is a lot of monthly movement and it must be very hard to establish the trend here.All the same, when you look at it in context, August 2007 doesn't seem to me to be a particularly exciting reading.

Subscribe to:

Posts (Atom)